For many homeowners, jewelry is more than just an accessory—it’s a symbol of life’s most meaningful moments. Whether it’s an engagement ring, a family heirloom, or a luxury watch, these treasured items deserve the right protection.

What many people don’t realize is that not all homeowners insurance policies provide the same level of coverage for jewelry. Understanding the differences between policy forms can help you avoid unexpected surprises when you need to file a claim.

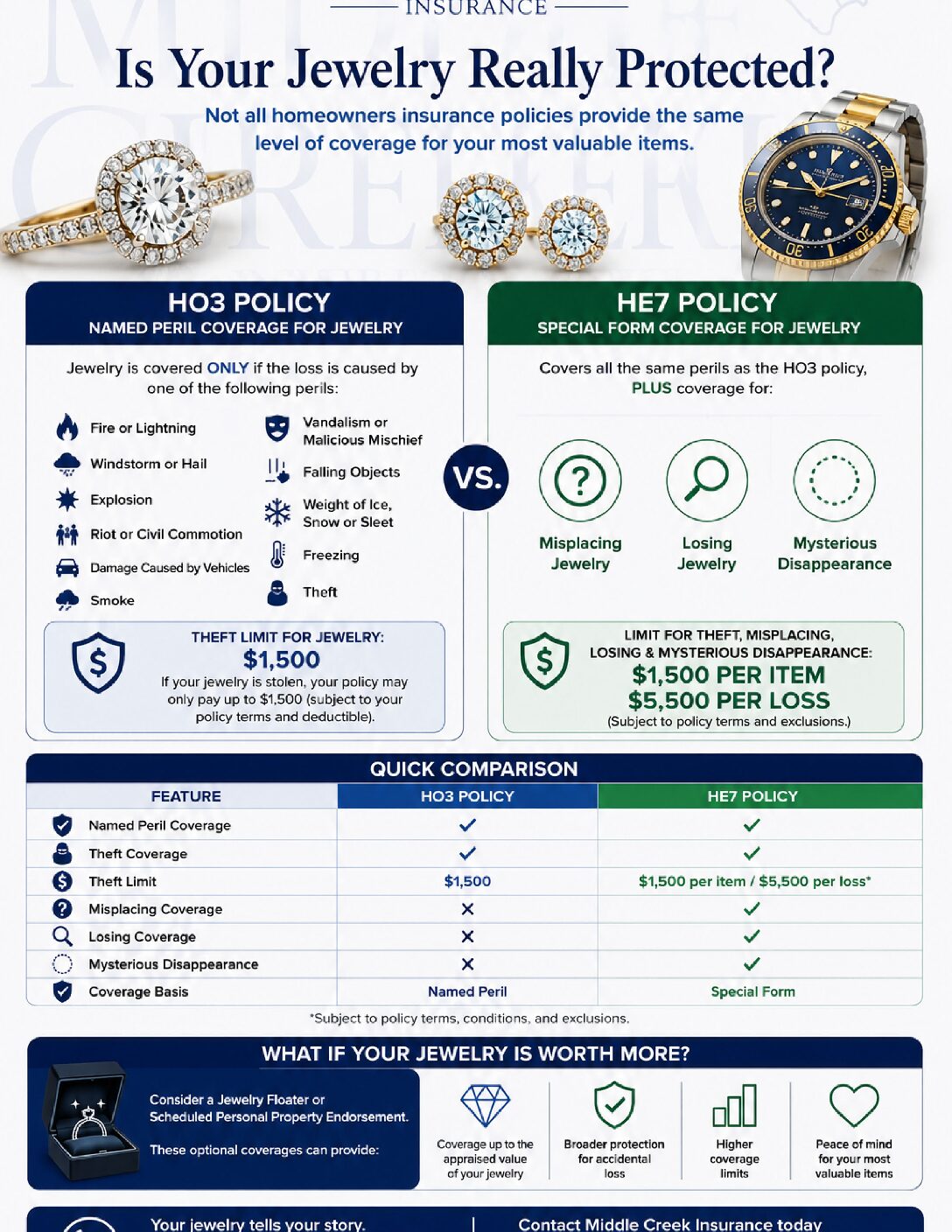

Jewelry Coverage Under an HO3 Policy

The standard HO3 homeowners policy provides named peril coverage for jewelry. This means your jewelry is covered only if the loss is caused by one of the specific perils listed in the policy, including:

- Fire or lightning

- Windstorm or hail

- Explosion

- Riot or civil commotion

- Damage caused by vehicles

- Smoke

- Vandalism or malicious mischief

- Falling objects

- Weight of ice, snow, or sleet

- Freezing

- Theft

While theft is covered, there’s an important limitation.

The theft limit for jewelry is $1,500.

If a valuable ring worth $8,000 is stolen, your policy may only pay up to the $1,500 theft limit (subject to your policy terms and deductible), leaving you responsible for the remaining loss.

Jewelry Coverage Under an HE7 Policy

The HE7 policy offers broader protection for jewelry by providing Special Form coverage for personal property.

In addition to the perils covered under an HO3 policy, the HE7 also provides coverage for situations that homeowners often worry about, including:

- Misplacing jewelry

- Losing jewelry

- Mysterious disappearance

Imagine taking off your wedding ring while gardening or traveling and later realizing it’s gone. With many standard homeowners policies, there may be no coverage if the loss wasn’t caused by a named peril. Under an HE7 policy, these types of losses may be covered.

The HE7 includes coverage for:

- $1,500 per item / $5,500 per loss for theft, misplacing, losing, and mysterious disappearance

Quick Comparison

| Feature | HO3 Policy | HE7 Policy |

|---|---|---|

| Named Peril Coverage | ✔️ | ✔️ |

| Theft Coverage | ✔️ | ✔️ |

| Theft Limit | $1,500 | $1,500 per item / $5,500 per loss* |

| Misplacing Coverage | ❌ | ✔️ |

| Losing Coverage | ❌ | ✔️ |

| Mysterious Disappearance | ❌ | ✔️ |

| Special Form Coverage | ❌ | ✔️ |

*Subject to policy terms, conditions, and exclusions.

What If Your Jewelry Is Worth More?

Even with the enhanced protection available through an HE7 policy, many engagement rings, luxury watches, family heirlooms, and fine jewelry collections exceed the built-in coverage limits.

That’s where a Jewelry Floater or Scheduled Personal Property Endorsement can make all the difference.

These optional coverages can provide:

- Coverage up to the appraised value of your jewelry

- Broader protection for accidental loss

- Higher coverage limits

- Peace of mind for your most valuable possessions

Protect What Matters Most

Your jewelry tells your story. Make sure it’s protected with coverage that matches its value.

Whether you’re reviewing your current homeowners policy, comparing an HO3 and an HE7 policy, or wondering if it’s time to schedule a valuable piece of jewelry, the team at Middle Creek Insurance is here to help.

Let’s review your coverage together and make sure your treasured possessions have the protection they deserve.

Disclaimer: Coverage varies by carrier and policy. Limits, exclusions, deductibles, and eligibility requirements apply. Please review your policy or speak with a Middle Creek Insurance agent for details specific to your coverage