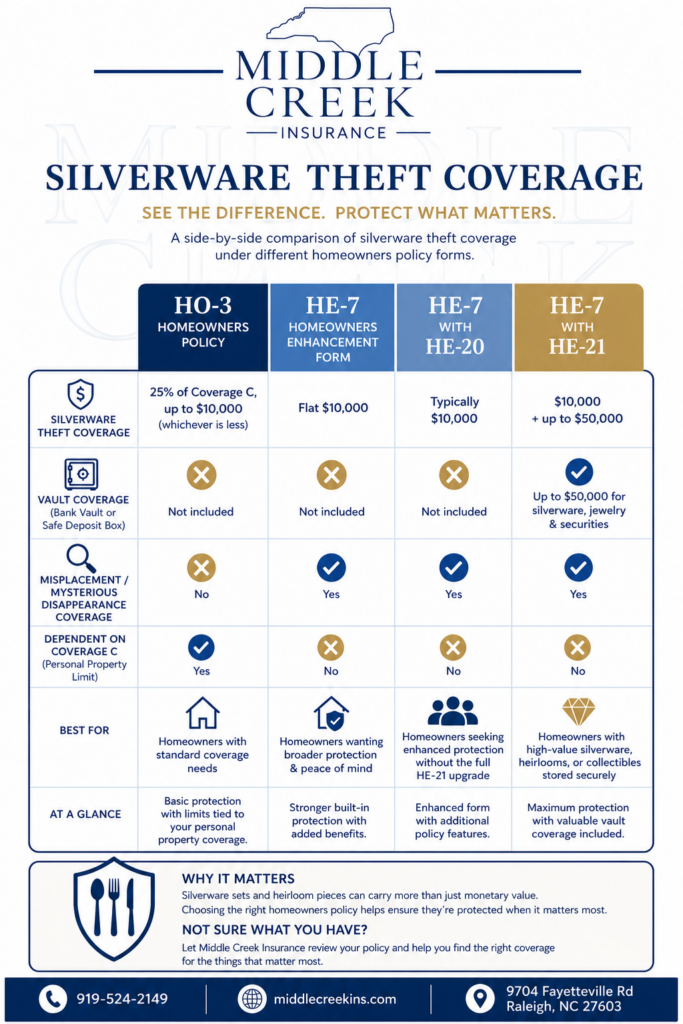

Silverware Theft Coverage: HO-3 vs. HE-7 vs. HE-7 with HE-20 vs. HE-7 with HE-21

At Middle Creek Insurance, we believe homeowners should understand the fine print—especially when it comes to valuables like silverware, sterling sets, heirloom serving pieces, and collectible flatware.

Many homeowners assume all theft coverage is the same, but that’s simply not true.

When comparing a standard HO-3 homeowners policy to an HE-7 form—and then adding endorsements like HE-20 or HE-21—the difference in silverware theft protection can be significant.

Let’s break it down.

Standard HO-3 Homeowners Policy

An HO-3 policy is the standard homeowners form many people carry.

For silverware theft, coverage is typically limited to:

25% of Coverage C (Personal Property), up to a maximum of $10,000

This means if your personal property limit is lower, your silverware theft protection may be much less than expected. Coverage also generally applies to theft only, not mysterious disappearance or accidental loss.

Example:

If your Coverage C is $40,000:

- 25% of Coverage C = $10,000

- Your silverware theft limit = $10,000 maximum

If Coverage C is $20,000:

- 25% = $5,000

- Your silverware theft limit = only $5,000

That can leave valuable inherited silver underinsured.

HE-7 Homeowners Enhancement Form

The HE-7 form offers stronger built-in protection than the standard HO-3.

For silverware theft:

Flat $10,000 limit

Unlike HO-3, this is not dependent on your Coverage C percentage. It also commonly includes broader protection for situations involving misplacing or mysterious disappearance, not just proven theft.

Why this matters:

If a family heirloom serving set goes missing after a holiday gathering, HE-7 may provide better claim handling than a basic HO-3.

HE-7 with HE-20

The HE-20 endorsement adds additional enhancement features depending on the carrier and policy structure, but it generally does not dramatically change the base silverware theft sublimit by itself.

Typical Silverware Theft Coverage:

Still around $10,000

The major advantage is usually improved overall policy enhancement rather than a major silverware limit increase.

This is a good middle-ground option for homeowners wanting broader protection without the full HE-21 upgrade.

HE-7 with HE-21 (Enhanced Protection)

This is where coverage becomes significantly stronger.

For silverware:

$10,000 standard theft limit + up to $50,000 for silverware, jewelry, and securities stored in a bank vault or safe deposit box

This added “vault coverage” is a major upgrade for clients with high-value collectibles or family heirlooms.

Ideal for:

- Sterling family heirlooms

- Antique silver collections

- High-value entertaining sets

- Estate valuables stored securely

Quick Comparison

| Policy Type | Silverware Theft Coverage |

|---|---|

| HO-3 | 25% of Coverage C, up to $10,000 |

| HE-7 | Flat $10,000 |

| HE-7 + HE-20 | Typically $10,000 |

| HE-7 + HE-21 | $10,000 + up to $50,000 in vault coverage |

Final Thoughts

The difference between these policies can mean thousands of dollars at claim time.

If your home contains:

- inherited sterling silver

- wedding silver sets

- antique serving pieces

- collectible flatware

- valuable family heirlooms

…it may be time to review whether your current homeowners policy truly protects them.

A standard HO-3 may look fine on paper—but an HE-7 or HE-7 with HE-21 could offer the peace of mind your valuables deserve.

Need a Coverage Review?

At Middle Creek Insurance, we help homeowners compare policies beyond just price—because coverage matters most when a loss happens.

If you’d like us to review your current homeowners policy and identify possible gaps in protection, we’re here to help.