At Middle Creek Insurance, we believe homeowners should understand not only what their policy covers—but also the limitations hidden inside the policy.

One commonly overlooked difference between homeowners policy forms involves coverage for cash, coins, bank notes, and similar valuables.

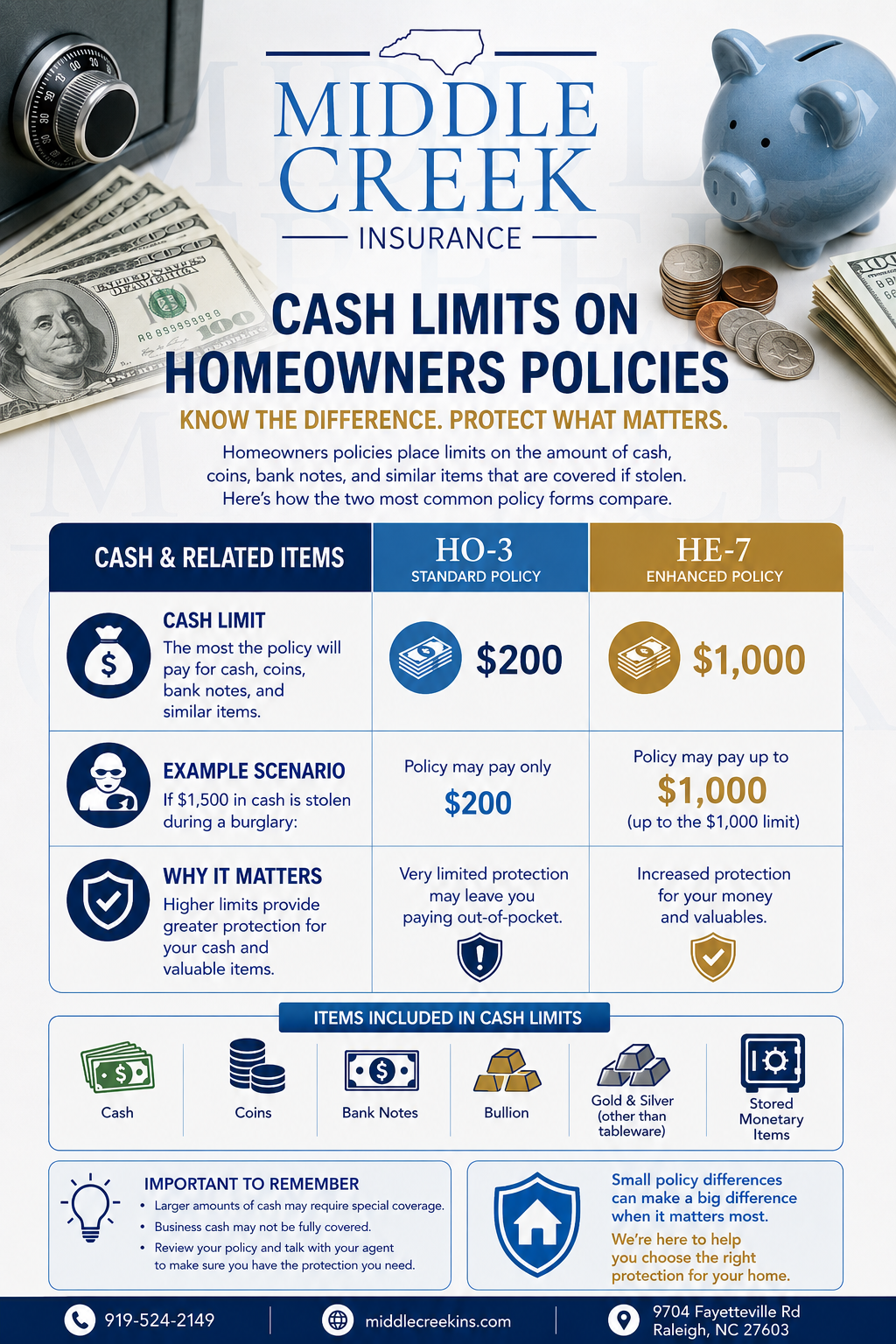

Many homeowners are surprised to learn that standard homeowners policies place strict limits on how much cash is covered after a theft or loss.

Let’s compare the difference between a standard HO-3 homeowners policy and an HE-7 homeowners enhancement form.

What Is the “Cash Limit” on a Homeowners Policy?

Homeowners insurance is designed to protect personal property, but certain categories of valuables have special limits.

One of those categories is:

- Cash

- Coins

- Bank notes

- Bullion

- Gold and silver other than tableware

- Stored monetary items

These limits apply primarily to theft losses and are usually much lower than your overall personal property limit.

Standard HO-3 Homeowners Policy

A traditional HO-3 policy includes a very limited amount of coverage for cash and related items.

Typical Cash Limit:

$200

That means if cash is stolen during a burglary, the maximum the policy typically pays is only $200—regardless of how much money was actually lost.

Example:

If a homeowner keeps:

- emergency cash at home

- savings hidden in a safe

- collectible coins

- stored cash for travel or family expenses

…and $3,000 is stolen during a break-in, the HO-3 policy may only pay $200.

Why This Matters

Many homeowners assume personal property coverage applies fully to cash, but special sublimits significantly reduce protection.

HE-7 Homeowners Enhancement Form

The HE-7 form improves many coverage areas—including the policy’s cash limit.

Typical Cash Limit:

$2,000

This is a substantial increase compared to the standard HO-3 form.

Example:

If $1,500 in emergency cash is stolen during a burglary:

- HO-3 may pay only $200

- HE-7 may cover the full $1,500 loss (up to policy limits)

Why HE-7 Matters

The increased limit can provide added peace of mind for homeowners who:

- keep emergency cash at home

- store collectible coins or currency

- want broader built-in protection

- prefer enhanced homeowners coverage

Quick Comparison

| Policy Form | Cash Coverage Limit |

|---|---|

| HO-3 | $200 |

| HE-7 | $2,000 |

Important Things to Remember

Even with enhanced coverage:

- Large amounts of cash may still exceed policy limits

- Collectible or rare coins may require special scheduling

- Business cash may not be fully covered

- Proper documentation is important after a loss

Homeowners should review their policy carefully to understand what is and is not protected.

Final Thoughts

Small policy differences can create major differences during a claim.

While an HO-3 policy provides basic homeowners protection, an HE-7 form offers broader built-in enhancements—including significantly higher protection for cash losses.

At Middle Creek Insurance, we help homeowners compare policies based on coverage—not just price.

Because when a loss happens, the details matter.

Need a Coverage Review?

Not sure what your homeowners policy actually covers?

Let Middle Creek Insurance review your policy and help identify gaps or opportunities for stronger protection.

📞 919-524-2149

📍 9704 Fayetteville Rd, Raleigh, NC 27603

Protect what matters most with coverage designed for real life.