If you own firearms, understanding how your homeowners policy responds to theft or disappearance can make a significant difference at claim time.

Many homeowners assume all firearms are covered equally under their policy. However, the coverage available under a standard HO-3 policy and an HE-7 policy can vary considerably.

At Middle Creek Insurance, we believe it’s important to understand these differences before a loss occurs.

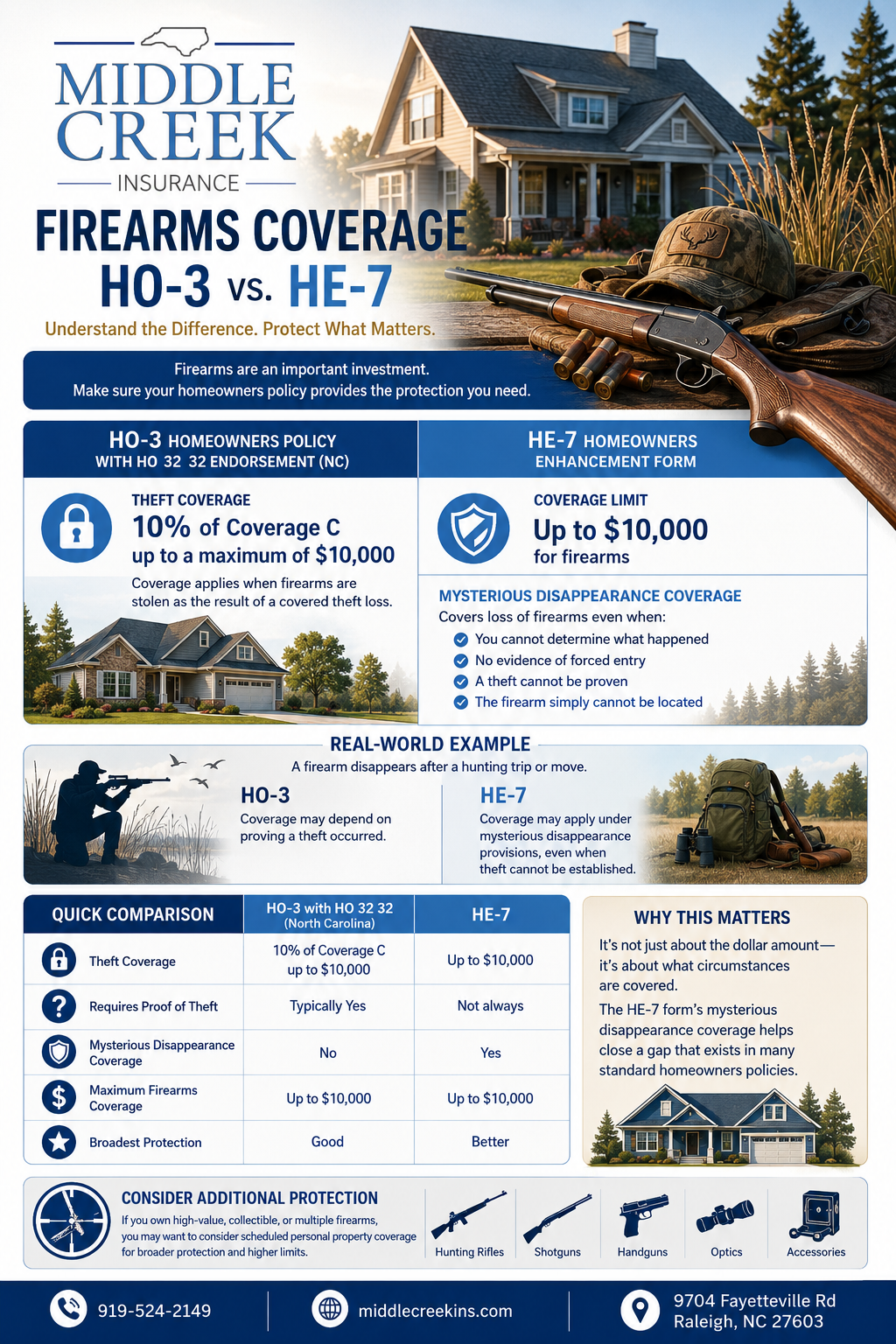

Firearms Coverage Under a North Carolina HO-3 Policy

Thanks to the HO 32 32 endorsement commonly attached to North Carolina HO-3 policies, coverage for theft of firearms is significantly enhanced from the standard policy form.

Theft Coverage Limit

10% of Coverage C (Personal Property), up to a maximum of $10,000

Example

If your Coverage C limit is $100,000:

- 10% of Coverage C = $10,000

- Maximum firearms theft coverage = $10,000

If your Coverage C limit is $50,000:

- 10% of Coverage C = $5,000

- Maximum firearms theft coverage = $5,000

This coverage applies when firearms are stolen as the result of a covered theft loss.

Firearms Coverage Under the HE-7 Form

The HE-7 Homeowners Enhancement Form takes protection a step further.

Coverage Limit

Up to $10,000

However, the biggest advantage is not necessarily the limit itself—it’s the broader cause of loss coverage.

Mysterious Disappearance Coverage

Unlike a standard HO-3 policy that requires a covered theft loss, the HE-7 form provides coverage for mysterious disappearance of firearms up to the policy limit.

This means coverage may apply even when:

- You cannot determine exactly what happened to the firearm

- There is no evidence of forced entry

- A theft cannot be proven

- The firearm simply cannot be located

For many firearm owners, this broader protection can be just as valuable as the coverage limit itself.

Real-World Example

Imagine a firearm disappears after a hunting trip, a move, or while multiple people had access to your property.

HO-3

Coverage may depend on proving a theft occurred.

HE-7

Coverage may apply under mysterious disappearance provisions, even when theft cannot be established.

This can make a substantial difference during the claims process.

Quick Comparison

| Coverage Feature | HO-3 with HO 32 32 | HE-7 |

|---|---|---|

| Theft Coverage | 10% of Coverage C up to $10,000 | Up to $10,000 |

| Requires Proof of Theft | Typically Yes | Not always |

| Mysterious Disappearance Coverage | No | Yes |

| Maximum Firearms Coverage | Up to $10,000 | Up to $10,000 |

| Broadest Protection | Good | Better |

Why This Matters

For many homeowners, the concern isn’t just theft—it’s uncertainty.

Firearms may be misplaced, lost during travel, disappear during a move, or simply become unaccounted for without clear evidence of theft.

The HE-7 form’s mysterious disappearance coverage helps close a gap that exists in many standard homeowners policies.

Firearms can be specifically scheduled (just like jewelry or furs or art). Let’s talk about how to do that for your collection.

Final Thoughts

At first glance, the HO-3 and HE-7 may appear to provide similar firearms limits. However, when you look beyond the dollar amount, the HE-7’s coverage for mysterious disappearance provides a meaningful enhancement.

Sometimes the difference isn’t how much coverage you have—it’s what circumstances are covered.

At Middle Creek Insurance, we help homeowners understand those differences so they can choose the protection that best fits their needs.

Need a Coverage Review?

Not sure how your firearms are covered?

Contact Middle Creek Insurance today for a homeowners policy review.

📞 919-524-2149

📍 9704 Fayetteville Rd, Raleigh, NC 27603

Because knowing your coverage before a loss is always better than learning about it afterward.