When shopping for homeowners insurance, many homeowners focus on premium costs and coverage limits. However, one often-overlooked feature can make a significant financial difference after a major claim: the deductible waiver.

At Middle Creek Insurance, we believe it’s important for homeowners to understand how different policy forms handle deductibles, especially when a large loss occurs.

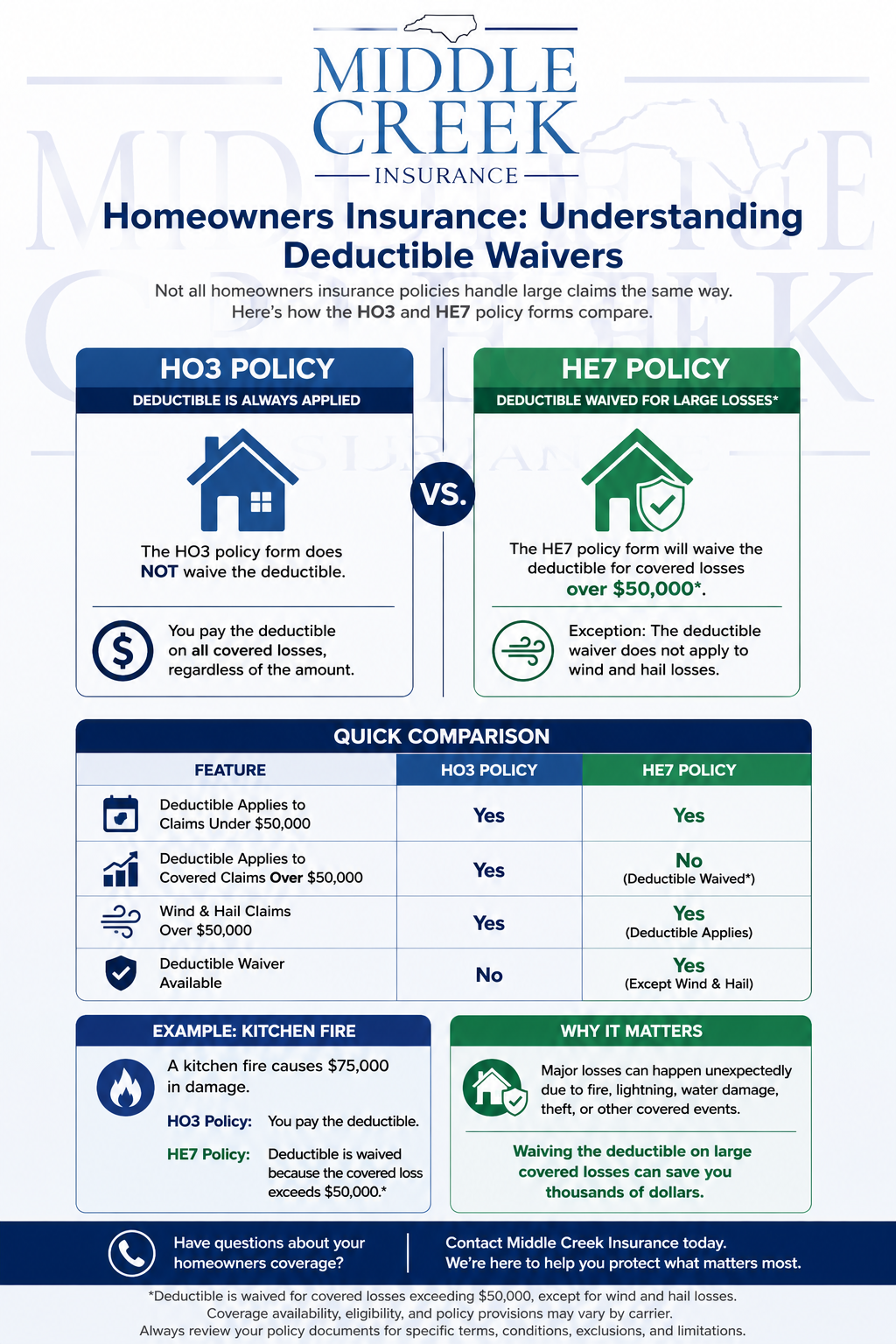

What Is a Deductible?

A deductible is the portion of a covered loss that you are responsible for paying before your insurance coverage begins to pay. For example, if you have a $2,500 deductible and experience a covered loss totaling $60,000, you would typically pay the first $2,500, and your insurance company would cover the remaining amount.

The HO3 Policy Form

The HO3 is one of the most common homeowners insurance policy forms available today. While it provides broad protection for your home and personal property, it does not include a deductible waiver feature.

This means that regardless of the size of a covered claim, the deductible will apply. Whether the loss is $10,000 or $100,000, the homeowner remains responsible for paying the deductible amount.

The HE7 Policy Form

The HE7 policy form offers an important advantage when it comes to large covered losses.

With an HE7 policy, the deductible is waived for covered losses exceeding $50,000, meaning you would not have to pay your deductible when a qualifying claim surpasses that threshold.

Important Exception

The deductible waiver does not apply to wind and hail losses.

For covered wind and hail claims, the applicable deductible will still apply, even if the total loss exceeds $50,000.

Why This Matters

Major losses can happen unexpectedly due to fire, lightning, water damage, theft, or other covered events. When repairs and replacement costs exceed $50,000, avoiding a deductible can provide meaningful financial relief during an already stressful situation.

Consider the following example:

Scenario: A kitchen fire causes $75,000 in damage.

- HO3 Policy: Homeowner pays the deductible.

- HE7 Policy: Deductible is waived because the covered loss exceeds $50,000.

The difference could save the homeowner thousands of dollars out of pocket.

Comparing the Two Forms

| Feature | HO3 Policy | HE7 Policy |

|---|---|---|

| Deductible Applies to Claims Under $50,000 | Yes | Yes |

| Deductible Applies to Covered Claims Over $50,000 | Yes | No |

| Wind & Hail Claims Over $50,000 | Yes | Yes |

| Deductible Waiver Available | No | Yes (except wind and hail) |

The Bottom Line

Not all homeowners insurance policies handle large claims the same way. While the HO3 policy form always requires the deductible to be paid, the HE7 policy form offers valuable protection by waiving the deductible for covered losses exceeding $50,000—except for wind and hail claims.

Understanding these differences can help you choose coverage that better aligns with your financial goals and risk tolerance.

If you’d like to review your current homeowners policy or explore whether an HE7 policy may be right for your home, contact Middle Creek Insurance today. Our team is here to help you understand your options and make informed decisions about protecting your most valuable asset.

Disclaimer: Coverage availability, eligibility, and policy provisions may vary by carrier. Always review your policy documents for specific terms, conditions, exclusions, and limitations.